President Biden signed an omnibus budget bill in December 2022, which included bipartisan legislation helping to make it easier for people to save for retirement. The SECURE (Setting Every Community Up for Retirement Enhancement) 2.0 Act builds on the previous SECURE Act law, which was passed in 2019. While not all of the changes in the SECURE 2.0 Act might affect you, it’s important to be aware of the changes. Here’s a quick look at some of the biggest updates.

Changes to Required Minimum Distributions (RMDs)

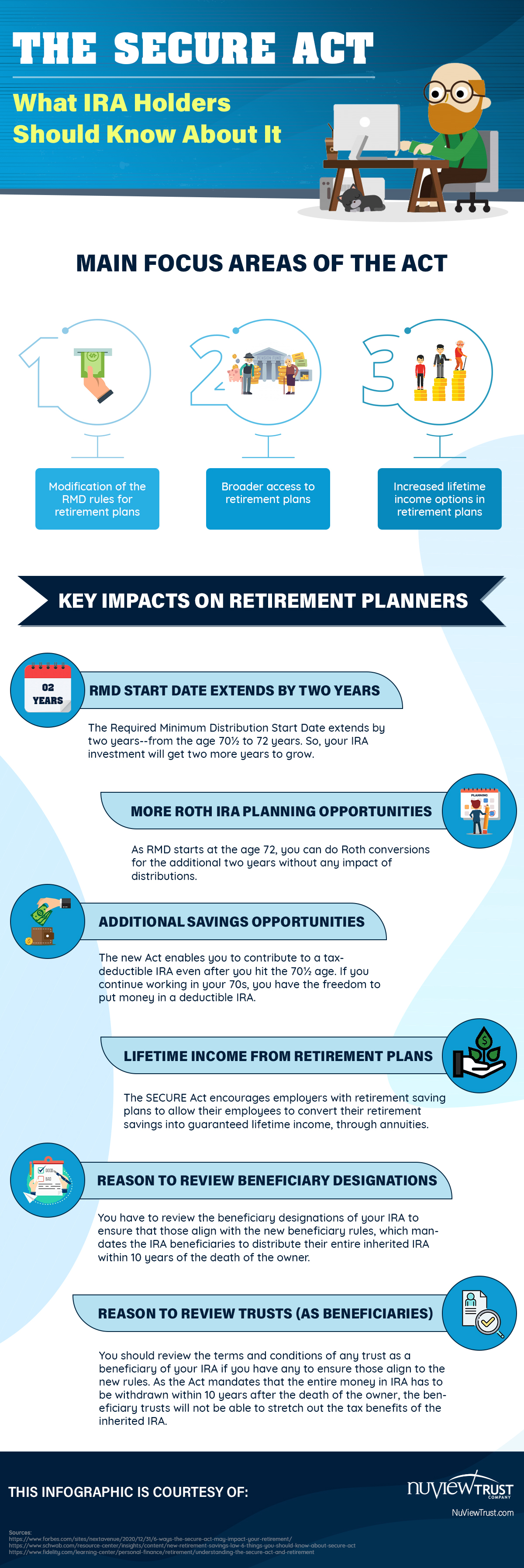

Many retirement accounts have Required Minimum Distributions (RMDs). The two most common types of accounts subject to RMDs are 401(k) and IRA accounts. The IRS wants to make sure that the money in these retirement accounts is withdrawn and spent (and therefore taxed). The SECURE 2.0 Act increases the age at which you are required to start taking withdrawals from your IRA or 401(k) plan. Prior to January 1, 2023, account holders needed to start taking RMDs at age 72, but as of the new year, that age increased to 73 and will increase to 75 in 2033.

An Increase in Catch-Up Contributions

Workplace plans (like 401(k) or 403(b) plans) and IRAs both have limits on how much you can contribute each year. To give workers who are closer to retirement age the ability to make sure they have enough saved, the new law allows older workers to make extra contributions. For example, workers age 50 and older can now contribute an extra $7,500 a year to the IRAs, up $1,000 from the previous maximum. The SECURE 2.0 Act indexes these amounts to inflation going forward. Starting in 2025, maximum 401(k) catch up contributions for workers ages 60 to 63 will rise to $10,000 annually.

Automatic Enrollment in 401(k) Plans

Even if you’re not particularly close to retirement, the SECURE 2.0 Act makes changes that may impact you. One such change is that new 401(k) and 403(b) workplace retirement plans will be required to auto-enroll eligible employees, starting in 2025. While this would not apply to existing 401(k) plans, it is likely a step in the right direction in helping Americans take steps to save for their retirement. Employees would be able to opt-out if they didn’t want to be enrolled.

Emergency Savings In A Roth IRA

A Roth IRA can be a great way to save for retirement, especially for younger people or those who are currently in low tax brackets. With a Roth IRA, you can contribute after-tax money which then grows tax-free in your account. As long as you withdraw the money for retirement (or a few other qualified events), you won’t have to pay federal income taxes on your distributions.

While a Roth IRA can be an attractive option for young people, it does come with some downsides. One downside is that it can be challenging to access that money if an emergency comes up. While there are some situations where you can withdraw money from your IRA without penalty, in many cases you’ll have to pay a 10% penalty and income tax on any withdrawals. The SECURE 2.0 Act allows Roth IRA participants to access up to $1,000 per year for qualified personal or family emergencies. It also allows workplace plans to set up a Roth-qualifying emergency account that can be funded with up to $2,500 per year.

A Way To Convert 529 Plans to A Roth IRA

A 529 plan can be a great way to save money for college and higher education expenses, but what happens if your child decides they don’t want to go to college? The SECURE 2.0 Act helps to answer that question by allowing you to rollover assets in a 529 plan into a Roth IRA as long as the account has been open for at least 15 years and does not exceed maximum contribution limits. There would be no tax or penalty to do such a rollover, and it is not treated as income for the beneficiary.

The rollover of a 529 plan to a Roth IRA would be considered a contribution to a Roth IRA and subject to the annual Roth IRA contribution limits. There is a maximum of $35,000 that can be rolled over from a 529 plan to a Roth IRA. Despite some of these limitations, this can be an attractive option for people who end up not using all of the funds in a 529 plan.

The Bottom Line

The SECURE 2.0 Act was signed into law in January 2023 and provides a number of updates to laws regarding retirement savings and finance. Make sure that you understand how these new laws might affect your specific financial situation. If you have questions, contact your trusted financial advisor to ensure that you keep yourself in the best financial shape possible.

The post 5 Things the SECURE 2.0 Act changes about retirement appeared first on MintLife Blog.

https://urbhy.com/5-things-the-secure-2-0-act-changes-about-retirement/?feed_id=8439&_unique_id=647c664f70222

إرسال تعليق